Social care providers in England have been thrown into the spotlight over the last year as they were hit by Covid-19. But providers of these vital care services are still too often ignored in the increasingly intense discussion around reforming our failing system. This report outlines the systemic problems with the way our market for social care operates, and argues that unless they are resolved, funding reforms alone will fail to deliver sustainable change.

This is the first of two reports by the Nuffield Trust looking at the provider market for social care. The second will consider the possible solutions and options for reform that can be learned from international settings.

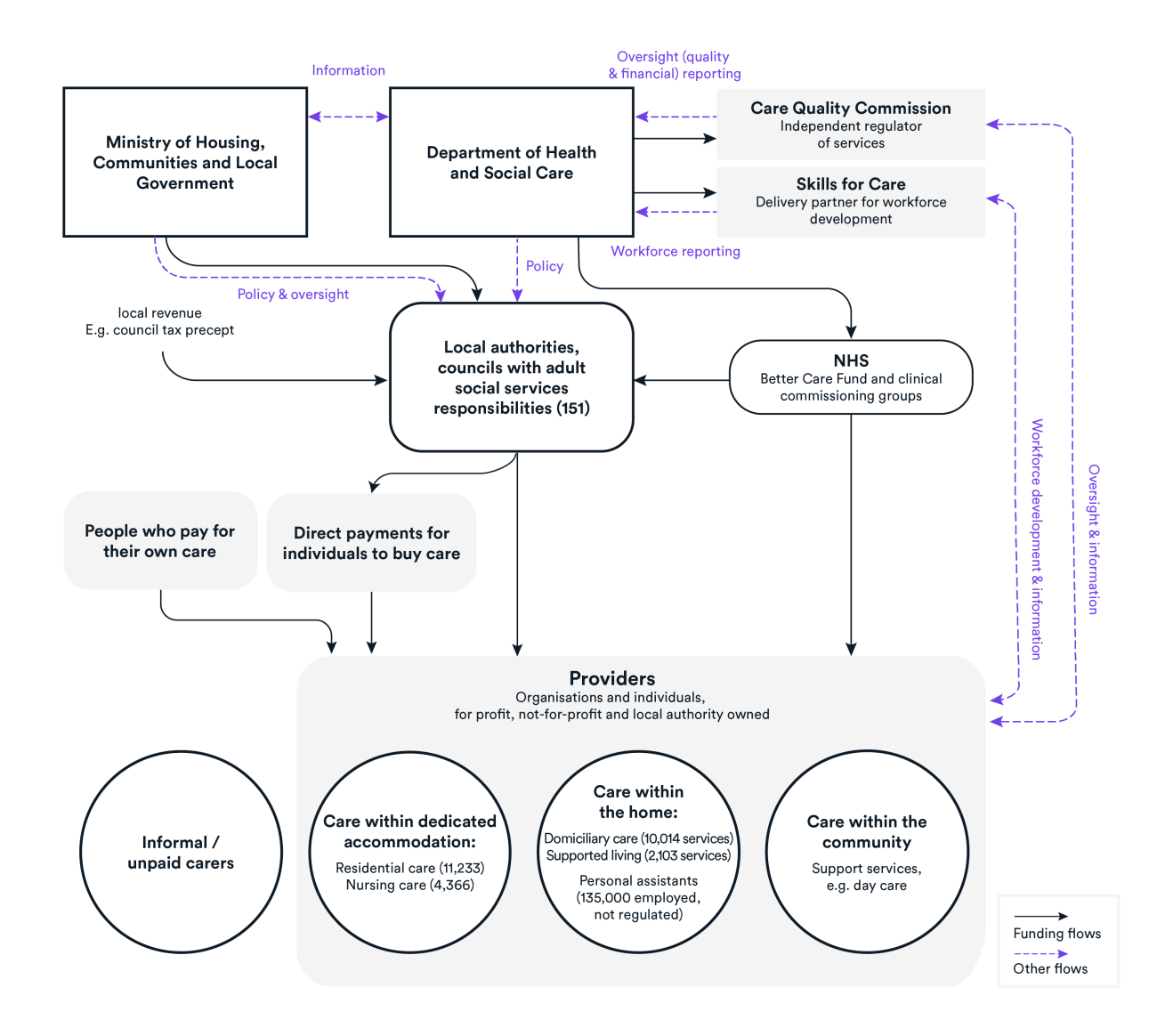

Key points

While there has been no shortage of proposals for reform over the last two decades, the singular focus on funding has ignored the fact that the provider market is overly complex and not functioning.

These are the main areas identified in the report which highlight the root causes of the market's instability:

Downward pressure on fees paid by councils creates uncertainty and variation

The lack of a long-term funding solution coupled with downward pressure on the fees paid by councils to providers over the last decade of austerity has created uncertainty and instability. Low fees have created inequity as providers charge more to self-funders than those funded by their council in order to remain viable. Regional variation in availability of care has widened as greater onus is put on councils to raise revenue from local sources.

Lack of effective ‘market shaping’ limits innovation and drives short-termism

Councils’ efforts at shaping and developing the provider market to suit the needs of the local population are hampered by a lack of a reliable data about providers and the people who use care services. A focus on balancing the annual budget, coupled with losses of experienced staff, has driven a shorttermist approach to purchasing individual care packages. This manifests in highly transactional relationships between providers and their commissioners and a lack of focus on innovation.

There are few proactive drivers of improvement or market management in the system

Quality of providers is generally high, but there has been little improvement among low performers over time. Commissioning is heavily transactional and the forces of choice and competition are limited by an asymmetry of information and a reluctance among people to switch provider, so there are few incentives or rewards for proactive service improvement. The CQC’s role in monitoring the financial health of the market is restricted to only the largest, ‘hard to replace’ providers. The CQC lacks the powers to take an improvement-focused role or to intervene to prevent financial collapse.

The ownership structure of many provider organisations creates instability in residential care

Opaque ownership and complex underlying business models of many large providers creates instability and uncertainty. The potential for making money through refinancing make it an attractive market for hedge funds, property investors and private equity funds. But these heavily debt-laden companies are highly sensitive to changes in the external environment and can quickly become unviable. In the event of a financial collapse, the provider bears no responsibility for care continuity – thus, there is no penalty for risky financial behaviour. Uncertainty over supply and continuity also arises from the business models of many of the smaller care home providers, which are often part of an owner’s pension pot and frequently sold to developers on retirement.

Social care has suffered from a lack of prioritisation within government

The Covid-19 crisis has highlighted the consequences of a sustained lack of prioritisation of social care, and a limited knowledge of the provider market, at the heart of government. Without a dedicated Director General between 2016 and 2020 and with a team of just 40, the Department of Health and Social Care’s lack of capacity to deal with a crisis on the scale of Covid-19 was plain. With accountability split between national and local government, a lack of good data upon which to base the response, and few established communication channels with providers, there was confusion about where responsibility lay or about the scale or type of need.

What is now needed from the current government is a vision for the whole system, and a strategy for achieving that. Only by taking a comprehensive approach that avoids the trap of focusing solely on funding will we be able to build a system that is stable, sustainable and resilient in the face of future pressures.

Suggested citation

Curry N and Oung C (2021) Fractured and forgotten? The social care provider market in England Research report, Nuffield Trust