What is PFI?

The private finance initiative (PFI) is a way of funding public capital projects – such as NHS hospitals – using private sources of money to pay for the upfront costs of their design, build and maintenance. The costs of this borrowing are repaid annually over many years, giving the private sector a profit and the NHS a new hospital.

PFI has been in the news lately, but is it a big thing in health?

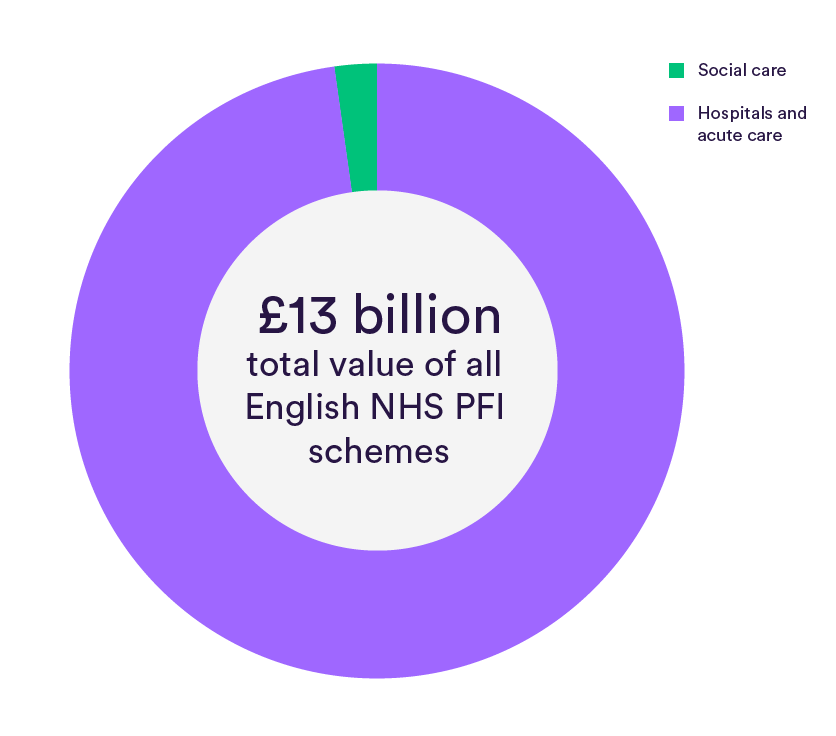

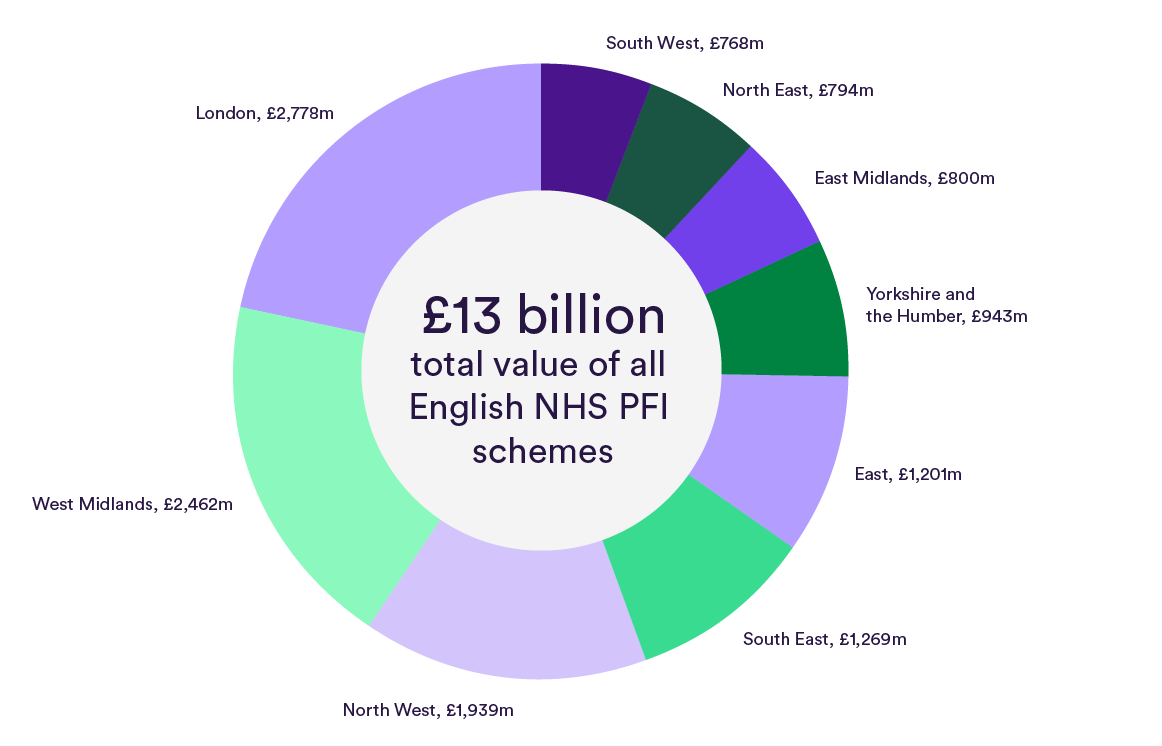

Pretty big. Across England there are 127 schemes – mostly now complete, with a few in construction, mainly in the NHS but also in social care. Their total capital value now adds up to nearly £13 billion.

Presumably these schemes vary a lot in size, though?

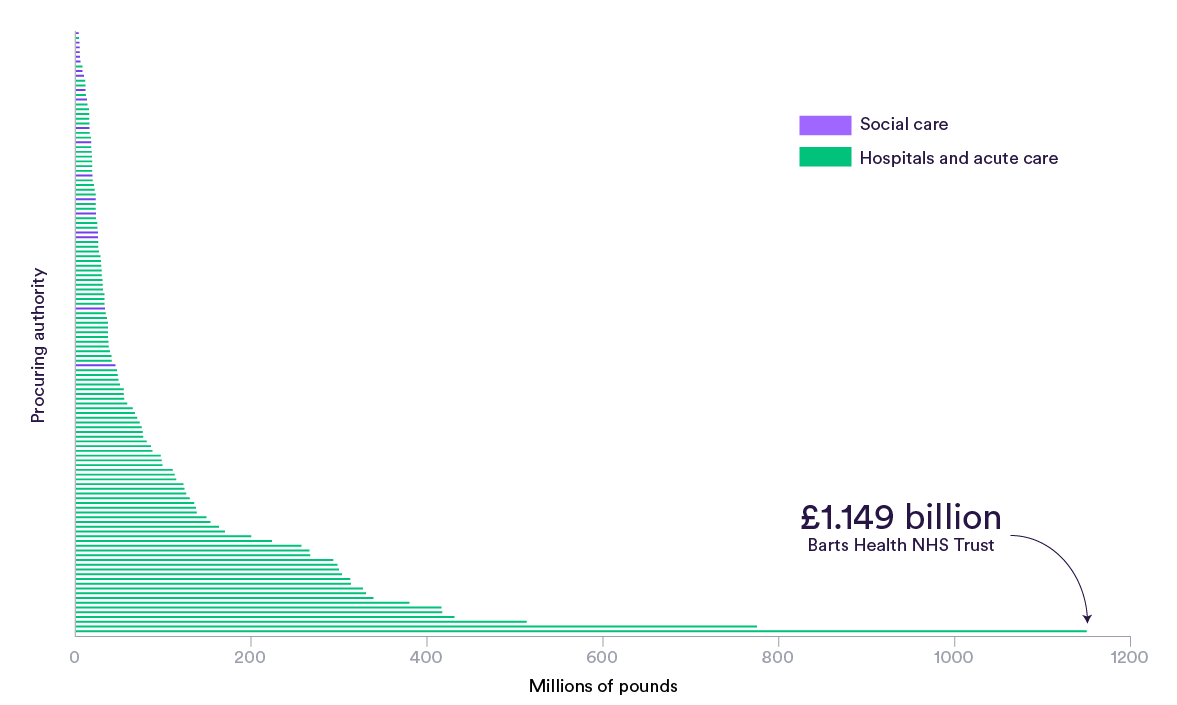

Yes they do. Many are relatively small – a new ward block, say. But some are large; Barts Health NHS Trust’s main PFI has a capital value of more than £1.1 billion.

Does borrowing the money to pay for capital works cost the NHS a lot in repayments?

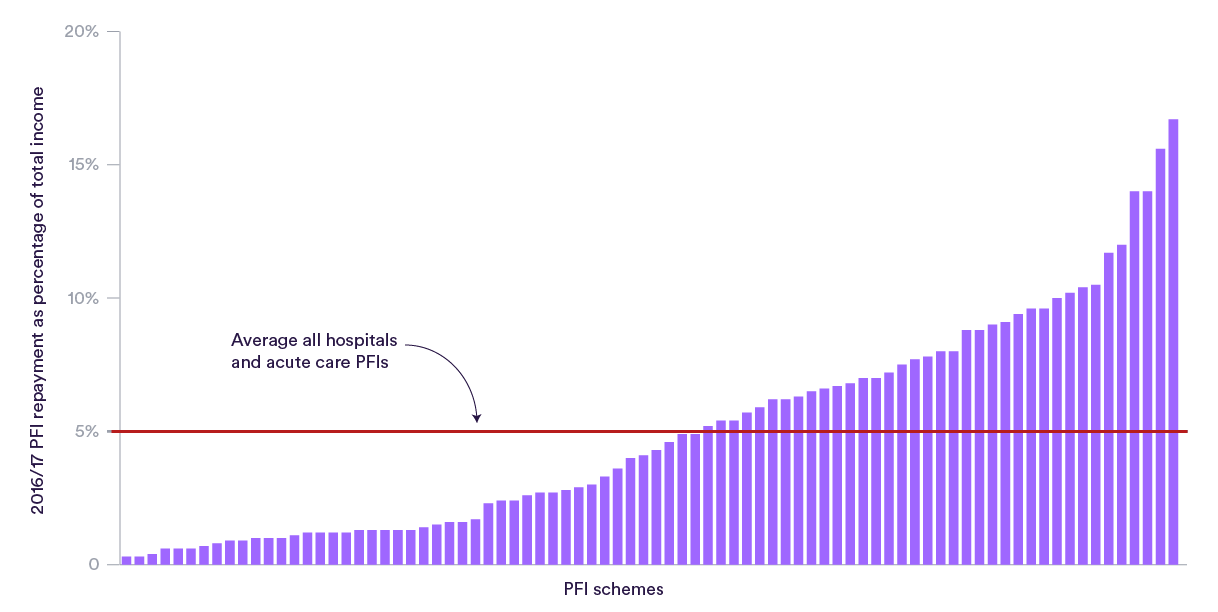

Quite a lot – though it varies from trust to trust in terms of the share of their total income. In absolute terms, Barts has the largest PFI scheme and its annual repayments amount to around 10 per cent of its income, whereas Sherwood Forest Hospitals NHS Foundation Trust paid 16 per cent of its total income in 2016/17 on its PFI charges. Repayments can vary – partly due to the different interest rate charges built into the deals, but also because many of the schemes also include the cost of running services such as facilities management, hospital portering and patient food. On average, 40 per cent of PFI charges relate to the cost of these services, although individual schemes vary from zero to 70 per cent.

How long will hospitals have to pay these charges?

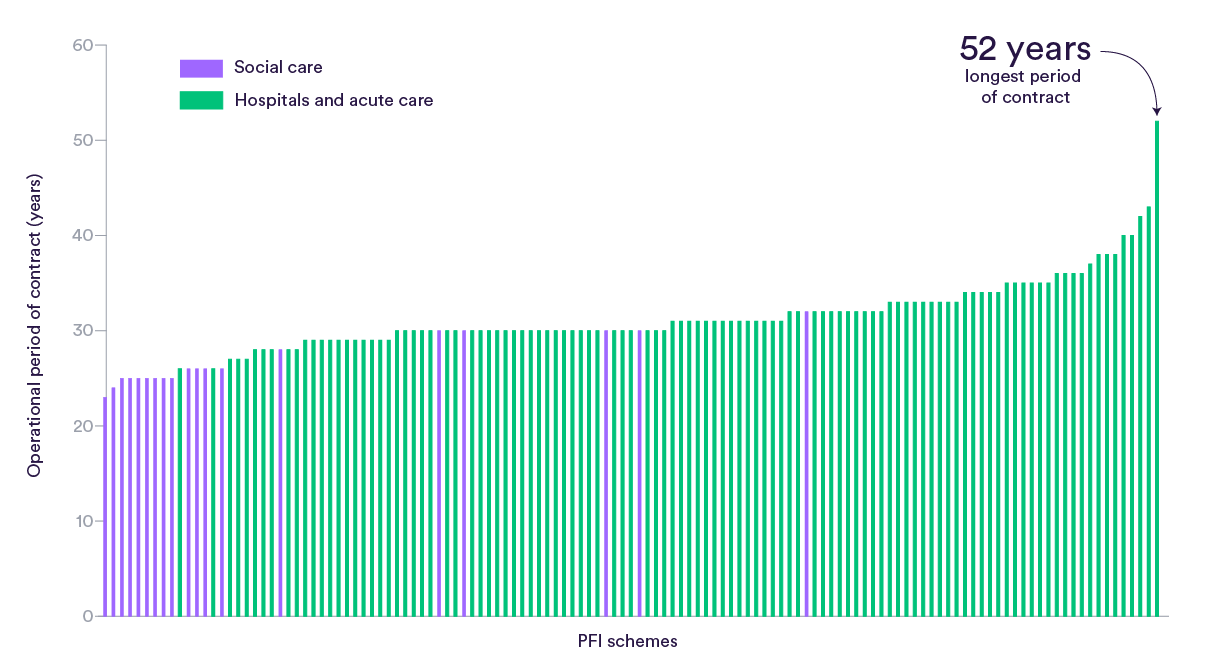

It depends on the particular deal that was made for each scheme. Many will last around 30 years, but the longest is 52 years – running from 1998 to 2050.

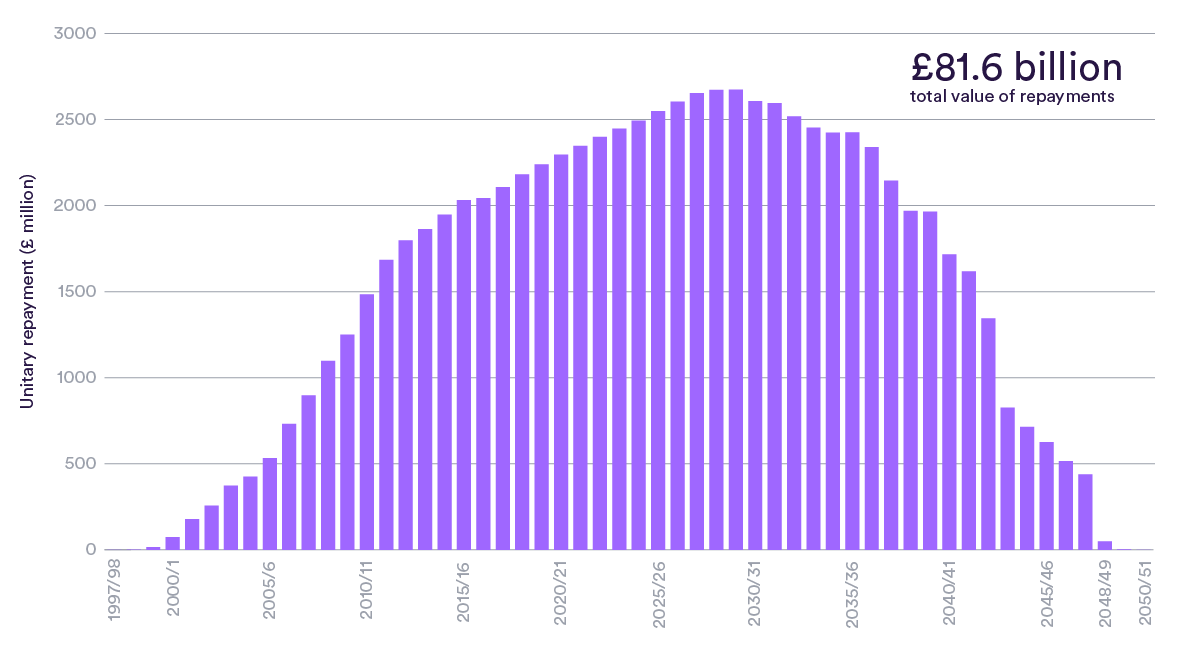

And how much will hospitals pay in total?

This year, total repayments will cost around £2.1 billion and will reach a peak in 2029. As older schemes come to an end, total repayments will start to fall as they approach 2049. In total, PFI repayments are expected to add up to nearly £82 billion.

How does the value of PFI schemes vary across England?

Of the £13 billion-or-so value of all schemes together, London has the highest share at around £2.8 billion, and the South West the smallest with £768 million. These figures partly reflect the different sizes of the NHS regions, differences in need for capital builds and so on.

So who’s involved with these deals on the ‘private’ side of PFI?

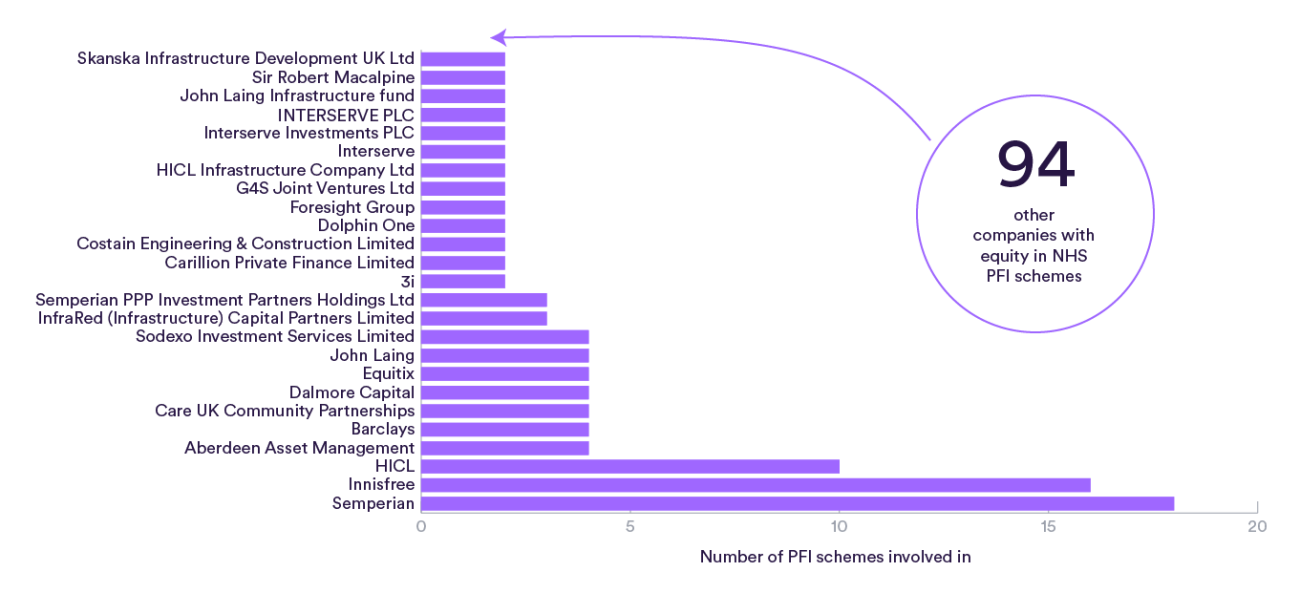

Every PFI has a separate ‘special purpose vehicle’ – a subsidiary company that helps keep assets secure from the parent company. It can also involve other companies in partnership – such as a bank and a construction company. This makes it a tricky question to answer, but in total there are around 120 separate organisations involved in PFI deals – some owning 100 per cent of the equity, others jointly owning smaller shares. And some are involved in more than one PFI scheme.

Why doesn’t the NHS save some money and just pay off these private groups rather than carry on paying every year?

That is an option in some cases. Tees, Esk and Wear Valley NHS Trust paid off its PFI scheme in 2011 and saved itself around £1.4 million a year in repayments. And in 2011, Northumbria Healthcare NHS Foundation Trust paid off its PFI deal by borrowing money from a local authority, thereby saving around £67 million over 20 years in repayments.

But in both those cases there were some special circumstances – not least the existence of an exit clause in the contract which allowed negotiations over settling the contract earlier than planned. Not all PFI contracts have such a clause.

Also, it’s not necessarily the case that a PFI scheme is poor value for money. It’s generally acknowledged that early schemes were not always good deals, but as the NHS gained more experience of PFI it negotiated better terms. Tees, Esk and Wear, for example, found that its more recent schemes were good value and left them in place.

Of course, the Government could find ways to end PFI schemes early on behalf of hospitals (and other public sector organisations), but the question is at what cost – not just in financial terms but in opportunity cost terms. Would it be money well spent, or could it bring more benefit if spent on something else?

There is no definitive answer on the cost of buying out PFI schemes – though some have suggested it could be funded in the same way as the Bank of England used quantitative easing, and others that it could amount to around 30 to 40 per cent of the total value of repayments into the future – equivalent to around £25 to £33 billion for all NHS PFI schemes in England.

What's the future of PFI?

As a way of financing capital schemes in the NHS, PFI might be running out of puff. Between 2011 and 2018 there will be 17 schemes which have or are planned to reach final construction; in the nine years from 2002 there were 92. One of the main reasons for this is the squeeze on NHS funding since 2010, and hospitals judging that PFI repayments are less of a priority than other spending (on staff for example) given pressures on the incomes.

The Nuffield Trust has asked a number of people to reflect on various issues around NHS estates, and we will be publishing these reflections as blog posts over the coming months. We’re also working with the Realisation Collaborative to bring together teams from a small number of local areas and national experts in a series of workshops designed to help the teams develop viable, implementable place-based estate plans. More information about these workshops can be found here.